Sequence Of Returns Risk – Why You Should Care

Sequence of returns take the chance of? Seems like something just old, abundant, retired individuals need to stress over … As long as I conserve up 25X my yearly costs as well as strike my FI number, I never ever need to bother with cash ever before once again, right?

Incorrect.

Series of returns threat is the No. 1 danger that can create very early senior citizens to lack cash. So take note my young FIRE good friends … this things is necessary.

A few of the mathematics can be complicated (it took me a while to cover my undersized mind around it), so I’m gon na attempt to discuss points as merely as I can, making use of rounded number instances. In this article I’m mosting likely to cover:

- What is this supposed “series threat” that retired individuals are babbling regarding?

- Why you may not care today, yet the 2nd you get to FI it will certainly be worrying.

- Why series threat frets the FIRE group greater than conventional retired people.

- Exactly how you can decrease your danger for when you struck FI!

Allow’s begin …

What Is Sequence of Returns?

Series of returns is essentially the order (series) in which favorable or adverse returns come time after time for your financial investment profile.

All of us understand the securities market will certainly have its ups as well as downs, and also market volatility is mainly out of our control …

Sometimes the marketplace will certainly increase, up, up, after that down.

Often it will certainly drop, down, down, after that up.

And also often it will certainly increase, down, sidewards, up, up, down, down, up, and so on and so on.

We typically do not care regarding what order the ups and also downs remain in, since we understand in the future, the stock exchange will primarily trend upwards. We generally just respect the ordinary financial investment return over an extended period of time.

The ordinary yearly return is what we make use of in our FIRE calculators, our retired life estimates, as well as nearly every long-lasting financial investment evaluation.

This may be alright when you are constructing riches, (actually, we are informed never ever to stress over when the marketplace accidents– simply maintain spending as well as persevere!)… however the series of returns has a massive effect when you really struck FI as well as begin taking withdrawals for retired life earnings.

Allow’s consider some series mathematics …

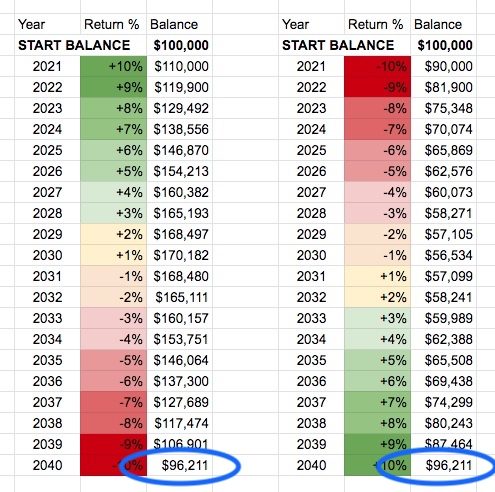

Sequence Example: $100k spent, left unblemished …

Here are 2 situations revealing a various series of returns over a 20 year duration. The left instance reveals a 10% return in year 1, after that a 9% in year 2, gradually shedding returns time after time. The appropriate instance reveals the specific contrary series of returns, beginning with -10%, after that -9%, and also acquiring a much better financial investment return every year.

Each instance begins with $100,000 attached worsening rate of interest.

As you can see, despite just how the series goes (from negative → excellent, or great → poor), both of these circumstances wind up with the very same quantity of cash. They both have $96,211 at the end of the 20 year duration.

As a matter of fact, you can mix/match these financial investment return portions in whatever order you desire. The ordinary return will certainly constantly amount to 0, as well as the retired life profile end result will certainly constantly be $96,211 after 20 years.

Currently, allow’s see what takes place when we begin to deduct cash year over year …

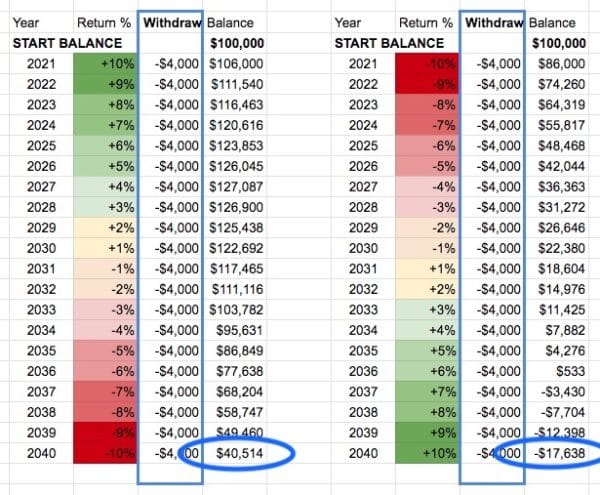

Sequencing Risk: Withdrawing $4k Each Year …

In these instances, we’re making use of the very same series as above. We’re additionally beginning with the exact same $100k preliminary savings, and also the only distinction is we’ll be obtaining $4,000 annually from the financial investment profile.

Wow, this is a quite incredible distinction. Beginning in a great market with points gradually becoming worse annually for 20 years, the profile worth left wing wound up with around$ 40k. However beginning in a negative market,

and also points gradually improving as well asfar better gradually, this financial investment profile on the right would certainly lack cash in year 15! This is series danger. Poor return years at the start of retired life

tosses the profile method off training course. Also if points frequently enhance later on, the great years later on can not offset the extreme damages that was performed in very early years. Keep in mind: My instances are certainly phony return numbers I offseted simpleness. If you desire some series instances utilizing genuine stock exchange returns, take a look at this calculator right here!.?.!! Different numbers, yet showing the very same factor:-RRB- Sequence of Returns Risk in FIRE vs. Traditional Retirement Currently allow’s speak concerning why the series of returns take the chance of really feels greater for the very earlyretired life and also FIRE area, vs. the typical standard retired person

. Commonly, individuals from the FIRE area retire when the marketplace is”high.”This is since their financial investment profile has actually expanded at a quicker rate than common, as well as since financial investment gains are substantially extra effective than their individual payments. I’ll highlight this with some

charts listed below. ** Fair caution: This is by no suggests a technological evaluation, this is simply a draft to show a point of view ** Here is a chart revealing the S&P 500 development over the last ~ 40 years … And right here, displayed in light eco-friendly dots, is when individuals retire generally. Generally, individuals retire when they transform a particular age. Someplace around 65

— 70 years of ages … which occurs each and every single year. Now, allow’s take a look at when individuals strike FI and also retire early, revealed with orange dots listed below … People typically retire early when they strike their FIRE number, despite their age. As well as lots of people strike their FIRE number throughout exceptional economic situations, when their profile has actually had awesome development. Again, this is an extremely simplistic as well as extremely overstated picture … If you wan na see a much better determined chart of endogenous retired life timing, look into this message from Early Retirement Now! It would certainly show up that anybody retiring on top of a booming market is doomed! That’s not always the situation. Even if you have a collection of favorable returns, it does not suggestit will certainly be adhered to by large adverse returns. Yet, checking out the orange dots, can you see why individuals retiring very early may be really feeling a little bit a lot more subjected to series danger? The various other variable that substances this problem is durability danger

. Early senior citizens require their retired life financial savings to last them a lot more years than typical retired people. The reality is, anytime

you retire, every person needs to prepare in advance for series danger. Below’s a couple of methods we can find out to reduce the influenceof negative very early financial investment returns. Initially, a fast note on risk-free withdrawal prices … The 4%Rule and also Safe Withdrawal Rates in Retirement It’s vital to keep in mind

that the 4 %regulation has a great deal of series of return danger reduction currently integrated. The man that developed the 4 %risk-free withdrawal price researched every one of the previous series

as well as market returns information from 1925 to 1995. His research ended” If background is any type of overview for the future, after that withdrawal prices of 3%and also 4% are very not likely to wear down any type of profile of supplies as well as bondsthroughout any one of the payment durations “This makes me really feel respectable

, however not 100% positive. Background is a good overview for the

future, however it’s not constantly precise.(2020 has actually shown this real– we’ve experienced lots of historical firsts this year

). So although the 4% guideline was developed to stand up to poor sequencing threat, many people call it a”standard,” or “guideline.” It should not be taken asscripture. HandlingSequence of Returns Risk The quickest means toremain in an extra comfy setting in retired life is to construct a somewhat larger savings. This seems like a piece of cake, however if you’re young and also in the

wide range build-up stage, why not remain there a little bit longer as well as develop on your own a barrier? Think about conserving 33x your yearly invest, rather than 25x. This decreases your withdrawal price to 3%, as opposed to 4%. Take into consideration inflating your future budget plan numbers a little bit, to ensure that in case

you have an instant market collision you can just invest much less than you were preparing for, without influencing your way of life. When determining future forecasts, make use of traditional

development numbers and also represent more than normal rising cost of living. You do not wish to get in retired life with the outright bare minimum conserved. You’ll rest far better recognizing you have over-prepared as well as have much less threat. An additional method to intend in advance is to maintain a huge cash money book container when you retire. 1, 2, or perhaps 3 years of living expenditures kept in cash money can be made use of for costs rather than taking outfrom your profile in down years. This might appear stupid, due to the fact that holding cash in money implies it’s not helping you, so your profile is

- expanding at a reduced ordinary return. Yet, the objective in retired life is not to collect riches as rapid as feasible any longer, it’s to protect funding so it can maintain feeding you– permanently. Trading a reduced return for reduced danger deserves it

- . Set revenue properties are one more device you can utilize to reduce the effect of series danger. This is extra better than the cash money container suggestion, since it has a much better risk-adjusted return. You can buy bonds or annuities that give a set retired life revenue quantity regardless of what the marketplace efficiency is. Once more, these kinds of financial investment cars have

a reduced return, however can deserve it to reduce the threat. Last but not least, a more comprehensive property allowance can assist in handling series of returns threat. Utilizing rental residential or commercial properties, for instance, you might rely on favorable rental capital to offer a section of your retired life revenue, in which situation you’re depending a little much less on market profile withdrawals. Strategy Ahead for Less Risk in Retirement! It’s amusing … As we are building up riches we are shown never ever to attempt as well as”time the marketplace.”It does not matter if the marketplace is misestimated or underestimated, we are motivated to maintain buck price balancing with every remaining cent we can manage.

Full speed in advance! However, this mindset requires to alter as well as develop as we obtain closer to reaching our FIRE number. Reducing danger and also protecting our tough made resources is necessary– specifically in the very first couple of years of retired life. Various other fantastic reviews I located while excavating around:”Buffer Asset” by PhysicianOnFIRE Ultimate Guide to Safe Withdrawal Rates by Big ERN PS”It’s never ever a poor suggestion to speak with a monetary expert as well as have them check your retirement and also assistance in handling series of returns threat. Their devices and also retired life calculators are extremely comprehensive! Pleased Monday, y’ all. Have an awesome week!

-

Bad Excuses to Spend Money 🤷️

What’s even worse than enjoying your close friends invest cash on crap ...

![]()

The Rubik theme is the best Premium WordPress Themes that perfect for news, magazine, personal blog, etc.