Should we go for a 15 year or 30 year mortgage?

Morning! Wan na ask your suggestions momentarily, however allow me strike you with a fast condition of where we remain in our house buying trip up until now as I understand you’re on the side of your seats over there;-RRB- The Mrs.

- has actually eliminated the back up concept of leasing so we’re currently 100% on for owning!Which I * believe

- * I’m alright with currently, however still a little bit worried naturally because it’s all occurring so quickly …

- Although I will certainly claim that we obtained close with * 2 * residences thus far, which offers me wish that the “appropriate one” is around simply around the corner!And we still

- have about 2 months to secure one in heading right into peak period right here, so I assume we ought to still be all right and also not need to stress over resolving right now (I simply desire we understood in advance * which * residences will certainly be beginning the marketplace so we can make the most effective telephone call!)

- On the other hand, it likewise feels like we’ve gotten in a * vendor’s market * currently with homes flying off the racks within 48 hrs, which indicates when we DO discover the one that fits our household we need to go full blast as well as defend it which ideally does not indicate tossing even more cash at it (which I decline to do, so the Mrs. far better have a much better back up strategy!!:-RRB-)And finally, we’ve broadened our target neighborhoods currently from one location to 2 locations we enjoy, so with any luck that need to make the choices much better also, although the initial one is still the closest as well as precious to my heart considering that a buddy as well as her youngsters live there …

So that’s where we’re at in the meantime … And I obtained ta claim, it’s an unlike simply a month ago of me FREAKING THE HELL OUT! Haha … It’s outstanding just how quick you can adjust to things when it shows up in life!

So go on sending out over favorable feelings please!! I’m enthusiastic our home is around!!

And in the meanwhile, it’s been head down in the * monetary * element over right here which need to be not a surprise to any individual that it’s been one of the most enjoyable component of the procedure;-RRB- After obtaining pre-approved via 2 various areas until now (USAA as well as a home loan broker advised by our real estate agent), it resembles we’re floating in the $650k-$800k variety of what we can “manage” based upon their evaluations, which certainly has absolutely nothing to do with what we can REALLY pay for, however a minimum of looks excellent theoretically;-RRB- Our real spending plan is in fact closer to $350k, and also may also drop to $330k relying on which location we wind up in, and also I’m really feeling respectable concerning that given that it suggests our home mortgage will certainly remain in the mid $200’s after we plunk down 20%.

Which leads us to today’s inquiry of whether it’s wise to go with a 15 year home mortgage and also conserve THOUSANDS on rate of interest in addition to a quicker settle, or maintain it wonderful and also secure with a 30 year and also a lot reduced repayments in instance cash’s limited some months/years?

I’ve hinted in previous short articles that I was established on the 15 year because we can luckily manage it and also it’ll just press me to repaying the home loan quicker, nevertheless remarkably I’ve obtained a couple of remarks from individuals I appreciate on just how the 30 year is a far better alternative to go. Regardless of the cost savings!

Right here’s one of them I’ll select, even if it originates from a monetary reporter and also writer that you would certainly anticipate to claim the contrary;-RRB- Per, Kathy Kristof:

I guarantee to quit standing out off hereafter … BUT … Buy a residence that you can manage with a 15– year home loan, however obtain the 30-year home loan. Why? You can pay it off in 15 years, if you desire. Yet, if something fails– you shed a task; have a large economic dilemma that requires to be dealt with, and so on– the 30 year home mortgage provides you the adaptability to fall to the less costly repayment, without threatening your residence.

Individuals obtain captivated with the suggestion of conserving all this cash with the 15– year car loan. However the rates of interest on this funding is just somewhat less expensive than the rates of interest on the 30-year financing. And also for that minor differential, you purchase on your own a TON of versatility. Once again, there’s no charge for settling a 30-year financing in 15 (or 10 for the issue), yet you do not need to … Enamored– hah! That’s me

!:-RRB- But I’ll settle on her factors of versatility right here, as that’s specifically the car loan we had ourselves the very first time around and also it behaved to be able to make additional repayments whenever we desired however weren’t compelled to. Not that we understood what we were doing at that time anyways, haha … We actually purchased a residence without any cash down and also funded 100% of it(!!! )But I do ask yourself if currently, with over 10 years of riches

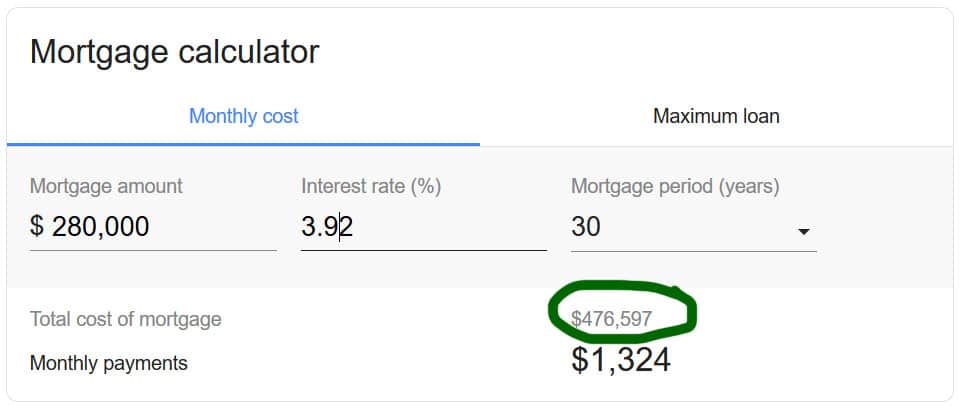

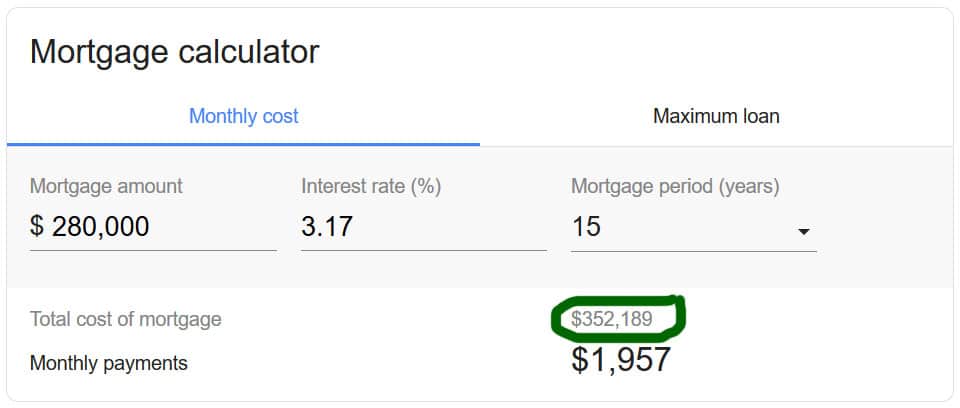

structure as well as * discovering * under our belts, we can much better endure the volatility of life for many years? As well as if so, would not it be finest to make the most of the cost savings? Kathy’s right that the 15 year prices are just “a little more affordable”than 30’s, however a portion of a portion factor– or in our situation when I initially obtained priced estimate– virtually.75 %of a factor!– can still make a helluva distinction over the long-term! Have a look at this fast contrast off google’s home mortgage calculator I simply did to place it in far better point of view … I’m making use of$280,000 as the home mortgage given that we’re taking down 20%, and also I left the default rate of interest alone because it looks around ideal anyways w/ our credit report: 30 year home loan @ 3.92%( A total amount of$476,597– insane!!!) )****** 15 year home mortgage @ 3.17

%( 0.75%

much less than the default price)

As you can see, that’s not specifically “somewhat less expensive!” Haha … We’re chatting a distinction of paying an overall of $476,597 with a 30 year or an overall of $352,189 with a 15! That’s $124,408 much less!!

And certain, you can still pay even more off each month and also tear down that interest/time significantly, yet you’re still losing despite paying * the exact same quantity * each and every single month like w/ a 15:

30 year home loan @ 3.92%

(paying an added $633/mo)

(through mortgagecalculator.org)Now this course obtains

you a LOT better, conserving you an added $98,576.49 and also practically 14 years off the initial 30 year!, nonetheless you’re still around$ 26,000 brief contrasted to sticking to the initial 15. And also certainly, this thinks that you’re certainly adding that$633/every month also as well as not being attracted or compelled to draw away! Which is a whole lot much easier to claim than do;-RRB- And that’s truly the heart of this Big Question at the end of the day … Is the financial savings of

$26,000–$124,000 a far better wager than the versatility of reduced settlementsextended throughout a longer time period? Or is it far better to play it risk-free, understanding fairly well that life does not constantly exercise as most of us strategy? With a 15 we’ll be investing a little bit greater than we are currently in lease( $2,300 )when you build up the insurance coverage as well as tax obligations as well as whatever else(those computations weren’t represented in the above instances ), however I seem like we have sufficient possessions to draw on nowadays than we did at that time if actually life actually did obtain so alarming? As well as worst instance God prohibited among us passes away, our$ 350,000 insurance coverage must be ample to cover the staying car loan! I’m undoubtedly leaning in this way, however I’ll confess Kathy as well as gang have obtained me 2nd thinking, haha … But that’s once again why I require your aid today !! To aid me place points in far better point of view, specifically if I’m missing out on something?? Because I truly can not overcome those ridiculous financial savings !!:-RRB- So inform me– have you

ever before attempted a 15 year home loan prior to? Or any type of various other much shorter terms? Just how did it wind up helping you ?? On the other side, just how are your 30 year home loans opting for every person rockin’those? I may not constantly concur with every person’s point of view, yet I check out and also value EVERY LAST ONE as well as such as to believe it makes me a far better general individual! Haha. So allow me have it !! Tell me what you would certainly do if you remained in my setting? I require extra outdoors guidance! Say thanks to youuuuuu … UPDATE: Here

‘s what we wound up choosing:-RRB-

-

Bad Excuses to Spend Money 🤷️

What’s even worse than enjoying your close friends invest cash on crap ...

![]()

The Rubik theme is the best Premium WordPress Themes that perfect for news, magazine, personal blog, etc.