Should I Refinance My Rental Property?

With rates of interest so reduced now, a concern on every house owner’s mind is,” should I re-finance my home mortgage? “As well as what concerning doing a re-finance on a rental home? It takes a reasonable quantity of initiative to refi– it’s much like getting approved for a new funding. There’s additionally large closing prices as well as costs … Is all that cash and also time worth it for a reduced rates of interest? The good news is, the net has clever calculators to aid figure all this things out! Allow’s run some numbers on my present Texas leasing home as well as see what a theoretical car loan re-finance would certainly appear like

. Allow’s likewise consider a squander refi, simply for the hell of it. Existing home mortgage on rental home Initial financing quantity:$ 136,500 (today there’s$ 123,235 entrusted to settle) Current rates of interest: 4.125 %Loan term: 30 years( begun in

2015, so 25 years staying) Monthly settlement:$

- 662 monthly I sent out all my home details to a home loan broker, and also they were able

- to send me back a quote for an upgraded rate of interest price as well as closing prices for a brand-new 30 year repaired price home mortgage. This is under the presumption that I have superb

credit score (I do!), which my earnings might get approved for the financing( I really do not assume it will certainly). No matter, below’s the quote I jumped on Aug 13th: New re-finance financing quote Brand-new rate of interest: 3.65% Mortgage term: thirty years (begins a brand-new 30 years throughout once again) Closing prices: $7000 Financing quantity:$ 130,235 (existing impressive equilibrium +$ 7k closing expenses) New month-to-month settlement: $ 596 each month Currently,

prior to you begin barbecuing me

- and also contrasting my price to the

- awesome below 3% price you simply hopped on your house refi, please comprehend that a financial investment building finance is discriminated than an FHA car loan. Financial investment building finances have greater rates of interest( normally 0.5– 0.75% greater), as well as financial institutions have a bit greater closing prices, as well . Overall, this re-finance choice would certainly lower my month-to-month repayments by $66 monthly, and also include$ 7k to my total car loan quantity for shutting expenses. (I’m making use of a re-finance calculator offered on Realtor.com). Is this a bargain? Well, it depends upon myfinancial investment objectives … The objective of refinancing With a home mortgage on the residence you reside in, lots of people intend to pay for their financial debt aspromptly as feasible, lower their general rate of interest to the financial institution, or substantially reduced their regular monthly home mortgage repayment. These are the typical factors individuals re-finance. This

being a financial investment building, my objectives are a little various than a main home. I do not truly appreciate repaying the car loan early, neither do I mind concerning the complete passion paid over the life of the funding. My primary factor to consider is raising capital.This is the distinction in between the rental revenue

as well as my expenditures. So for me, the largest advantage of re-financing today would certainly be the decrease in the regular monthly home loan settlement. This would certainly be an additional 66 dollars in my pocket every month. Yet, it comes with a rate. I would certainly need to spend( or obtain) an additional$ 7,000 to accomplish this$ 66/m decrease. Aware over you can see it will certainly take

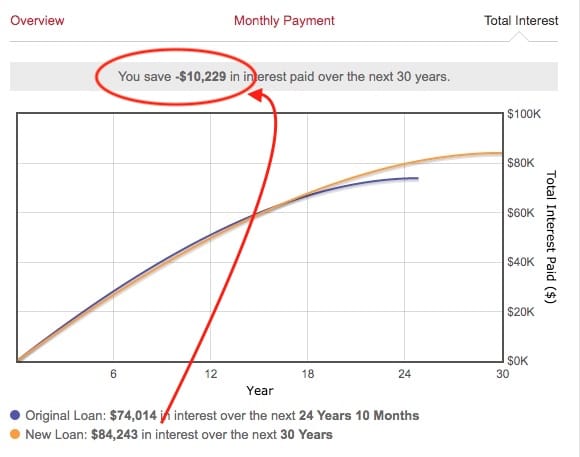

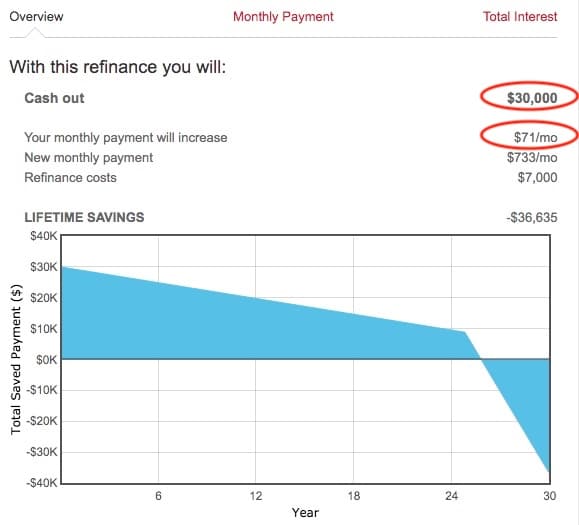

8 years as well as 10 months to get to a breakeven factor. At these numbers, I do not believe a fundamental re-finance make good sense now. Simply for enjoyable, have a look at the overall passion paid on the brand-new lending vs. the old lending. If I was to go on with this refi, as well as maintain the lending for a complete 30 years, I would certainly wind up paying an added $10,229 in home mortgage rate of interest over thecar loan term. Type of tricky! What regarding a squander re-finance? This rental residential property has actually valued in worth because I acquired it 5 years earlier. It deserved ~ $189k after that and also currently worth regarding $220k. This offers me an alternative to take out a few of the equity, while additionally re-financing to a reduced price.The majority of lending institutions will just lend up 75% of the worth on a financial investment building, so I require to make certain my car loan does not surpass $ 165k( 75% of 220k ). Allow’s see what the car loan would certainly appear like if I took out$ 30,000 in cash money: Cash out refi alternative Brand-new rates of interest: 3.65% Loan term: three decades Closing expenses:$ 7000 Car loan quantity:$ 160,235 (present equilibrium+ $7k closing expenses +$ 30k CASH OUT )New month-to-month repayment:$ 733 monthly Currently THIS is an actually fascinating alternative … Increasing my funding quantity by$ 37,000 would just set you back

me$ 71 monthly in greater home loan repayments. Where else can you obtain$ 30k in cash money today and also have it cost you just$ 71 monthly?Is this a bargain? Well, it still dependson my financial investment objectives! What could I finish with the added $30k if I had it in cash money today? Where would certainly I spend it, and also could I make greater than $71 each month from it over time? Most likely! I can stick it right into the stock exchange and also most likely make an excellent return

over time. Yet …

- Bad information: I most likely ca n’t get approved for a re-finance ideal now.:-LRB- The refinancing

- procedure is equally as tough as making an application for a new rental building funding. The car loan police officer will certainly brush via each and every single space and also cranny of my monetary life,

and also they most likely will not like what they see.:-LRB- I have a lots of the high quality required: My credit report is exceptional,my total assets is fantastic for my age, I have lotsof cash money books, and also my total financial obligation to equity proportion is conventional. Yet the largest worry they will certainly have is

my existing individual revenue as well as last couple of years of job background. I’m simply coming off a 2 year sabbatical, and also today my revenue covers my standard living costs, yet very little extra. I have 5 home loans presently (for 5 various services). As well as although all the month-to-month financial debts are conveniently paid by the inbound rental fee, a lot of standard lending institutions would like to know that my individual earnings can service my general financial debts. Some loan providers will certainly take into account inbound rental fee streams as an income source (perhaps at a minimizedprice ), yet it’s a challenging sell. Profile finance, exclusive cash borrowing, or industrial finance? There is some hope. I might make close friends with a little loan provider that prefers property investing. I might place on a match and also connection, collect all my documents, take a seat with the financial institution VP and also mathematically show to them that this squander refi would just raise my regular monthly expenditures by$ 71 monthly( I canabsolutely manage this!). Yet, because these smaller sized lending institutions manage ‘riskier’ car loans, they will certainly desire even more incentive for their financial investment. They will have a lot greater rate of interest– perhaps 2-3% greater– which places me waaaay back to the beginning of this entire mind … Will the brand-new home loan price they supply me deserve refinancing? Most likely not. In conclusion, refinancing is something I’ll continuously review. Yet now I believe I’ll maintain points as they are.:-RRB- TLDR; Summary A typical re-finance would certainly conserve me$ 66

monthly! However it would certainly set you back$ 7000, so the repayment is practically 9 years. A squander refi looks outstanding! I might take out$ 30k in equity. Regrettably I can not receive this( today )I’ll be reflecting on quickly as my earnings grows/stabilizes! I understand a number of you people most likely re-financed lately … Tell me your incredible success tales! Have you done a rental building re-finance? Any type of cash-out tales for reinvestment somewhere else?

-

Bad Excuses to Spend Money 🤷️

What’s even worse than enjoying your close friends invest cash on crap ...

![]()

The Rubik theme is the best Premium WordPress Themes that perfect for news, magazine, personal blog, etc.